What is distribution? See the BFI Screenonline

Turn to the FDA and watch these videos, starting with Matt Smith of Lionsgate:

On the FDA website www.launchingfilms.com : read the FDA Guide to Film Distribution https://www.launchingfilms.com/assets/FDA_Guide_to_UK_Film_DistributionMain.pdf

The FDA resources on Film Space http://thefilmspace.org/fda100/distribution/

http://thefilmspace.org/fda100/distribution/distributor

The electronic sell-through (EST) TV and movie market has grown since 2012 to more than $1 billion with EST sales now representing almost 14 percent of the 2013 physical and digital home video purchase. EST movie transactions grew 68 percent year-over-year in Q1 driving most of the total EST sales and accounting for 10 percent of all physical and digital movie purchases. Despite the improved growth of EST movies, EST TV show unit volume is still a much more significant part of the total EST market.

“Much of the growth in EST is being driven by new digital buyers being drawn into the market,” said Mark Kirstein, president of entertainment for The NPD Group. “Most of the 11 million EST consumers are purchasing digital transactions in addition to physical DVDs and Blu-ray discs; only a small percentage exclusively purchase digital.” The EST market is getting a boost as new multichannel video programming distributors (MVPD) and digital retailers join the market and new titles get early release windows. “Comcast joined Verizon as the second major MVPD to offer EST and we expect more to join the EST market moving forward,” said Kirstein. “EST will become an important complement to Video-on-Demand, TV Everywhere, and traditional pay TV services, as it drives incremental revenue and contributes to subscriber retention.”

Turn to the FDA and watch these videos, starting with Matt Smith of Lionsgate:

On the FDA website www.launchingfilms.com : read the FDA Guide to Film Distribution https://www.launchingfilms.com/assets/FDA_Guide_to_UK_Film_DistributionMain.pdf

The FDA resources on Film Space http://thefilmspace.org/fda100/distribution/

http://thefilmspace.org/fda100/distribution/distributor

THE FDA HANDBOOK 2018

FILM FESTIVALS

Markets and festivals

Distributors need to meet producers and agents in order to obtain the rights to films, and one key place where this happens is at trade events – international film markets and film festivals.

Distributors need to meet producers and agents in order to obtain the rights to films, and one key place where this happens is at trade events – international film markets and film festivals.

- a market, where distributors seeking to acquire product may meet with sellers (agents, producers, studios);

- a competition, where new titles may be screened to juries of filmmakers and awarded prizes. Such accolades flashed on a film’s poster can add prestige but may also be perceived by a more mainstream audience as not being for them ie. an ‘art house’ film;

- a high-profile platform where films can be showcased to influential media prior to release.

There are dozens of busy film festivals in towns and cities worldwide, but the main annual events attended by thousands of international film buyers and sellers, and almost as many journalists, are at Sundance (January), Berlin (February), Cannes (May), Venice (August) and Toronto (September). The annual American Film Market is another large gathering that takes place in November.

These events, each with their own personality, serve various functions:

Distributors sometimes choose to launch films at a suitable international festival, where critics and insiders may discover them and go on to champion them in early reviews and columns. The eyes of the film world and the mass media are focused on the leading festivals, such as Cannes on the French Riviera, which accommodates many premieres and junkets.

Most distributors need to have a ‘slate’ – a line-up of various films – to release in any year. Normally this would be a mix of different genres of films and the mix would depend on the distributor.

In the US, the studios often work with major producers and have on-going ‘first look’ deals on the films they want to produce. The studio will finance a chosen production, providing shooting and post-production facilities. In due course it will then distribute the film in the domestic market (US and Canada) and/or international (the rest of the world).

Occasionally, and most often with big-budget blockbusters, a studio may sell off the international rights to another distributor(s), to disperse the risk among more participants.

On its slate, a major studio will probably have a number of big-budget “tentpole” films, usually for release during a holiday period such as the summer or Christmas. They would probably also have a number of mid-budget films for release outside the holiday season.

The studio itself will have many projects in development – particularly franchise films (which we look at in week two) or adaptations of bestselling novels. So, as Sophie Doherty points out, the studio will know what it will be releasing in the years ahead and will have tentative opening dates for many near-future releases. You can see these in the forward planner section of FDA’s website, www.launchingfilms.com/release-schedule

Independent film distributors tend to take a different approach. They are resourced differently and will need to build their own slate title by title from various sources, as we have already seen. Some will have “first look” deals – where they can sign up for a film or pass on it, depending on their opinion of its prospects – thanks to long-standing business relationships with producers or agents.

To acquire films, distributors will often attend film markets. Various trade markets take place throughout the year, often associated with big film festivals. Sales agents such as Alison Thompson will meet distributors there to try to license films at concept, draft script, filming, post-production, or even at non-final or completed stages.

THE VALUE CHAIN

Overview of film distribution and exhibition monetization

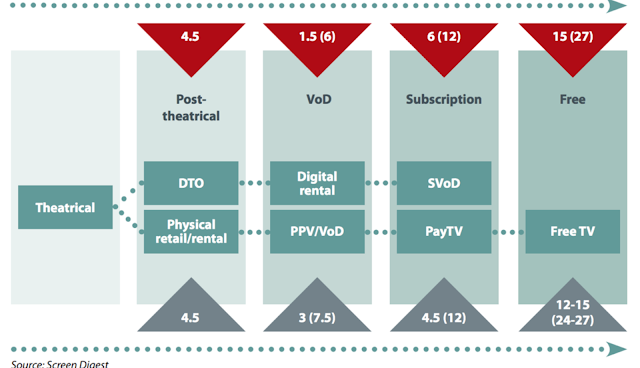

Cinemas are being squeezed by distributors giving them increasingly less time to show films exclusively. Six years ago the theatrical ‘window’ was shortened from six months to four months. Since then Hollywood studios have pressured exhibitors into accepting ever-shorter theatrical windows as they rush to recoup their investment in as short a time as possible from DVD sales, pay-per-view and other formats and outlets. Things came to a head in February 2010 when three UK exhibition chains refused to screen Alice In Wonderland after Disney announced it was releasing the film on DVD 12 weeks after the theatrical opening, rather than the industry standard of 17 weeks. While the typical four-month window is appropriate for Hollywood-style blockbusters, it is less so for smaller, independent films with a more limited P&A budget. There have been steps made towards innovation in this area – including for example the North American VOD release of Gareth Edwards’ Monsters (2010) one month before its US theatrical release. Windows experimentation is more relevant for low budget films because their box office visibility is generally lower and their theatrical runs are generally shorter. For example, Dogwoof, the UK documentary distributor, released the Academy Award-winning documentary Bill Cunningham New York on DVD just one month after its theatrical release to capitalise on publicity. For independent producers, the shorter the window between theatrical and other platforms the better: consumers can be alerted to the film’s availability on other platforms, capitalising on the theatrical release campaign and improving cash flow, while removing the need for a separate DVD marketing campaign.Global Film distribution windows (Months after theatrical)

Global Film distribution windows (Months after theatrical)Industry’s primary box office and home video sources of revenue

For any given film, box office receipts and home video sales (both domestic and international) account for an overwhelming portion of gross revenues. However, other channels, such as TV licensing and pay-per-view, as well as emerging platforms such as video-on-demand (VOD) and Internet downloads, also contribute a meaningful portion of a film’s total ultimate earnings over its life span. The table summarises the industry’s primary box office and home video sources of revenue.

Post-Theatrical

Download-to-own (DTO)/Electronic sell-through (EST) (After 4.5 Months)

Download to own is a concept of legally downloading movies to your computer via a network such as the Internet. It is a method of media distribution whereby consumers pay a one-time fee to download a media file for storage on a hard drive. Although DTO is often described as a transaction that grants content "ownership" to the consumer, the content may become unusable after a certain period and may not be viewable using competing platforms. DTO is used by a wide array of digital media products, including movies, television, music, games, and mobile applications. Generally to obtain movies this way a user must have a broadband connection and an account from an Internet distribution company. Typical companies under the model of DTO are iTunes, Film4oD, Distrify.The electronic sell-through (EST) TV and movie market has grown since 2012 to more than $1 billion with EST sales now representing almost 14 percent of the 2013 physical and digital home video purchase. EST movie transactions grew 68 percent year-over-year in Q1 driving most of the total EST sales and accounting for 10 percent of all physical and digital movie purchases. Despite the improved growth of EST movies, EST TV show unit volume is still a much more significant part of the total EST market.

“Much of the growth in EST is being driven by new digital buyers being drawn into the market,” said Mark Kirstein, president of entertainment for The NPD Group. “Most of the 11 million EST consumers are purchasing digital transactions in addition to physical DVDs and Blu-ray discs; only a small percentage exclusively purchase digital.” The EST market is getting a boost as new multichannel video programming distributors (MVPD) and digital retailers join the market and new titles get early release windows. “Comcast joined Verizon as the second major MVPD to offer EST and we expect more to join the EST market moving forward,” said Kirstein. “EST will become an important complement to Video-on-Demand, TV Everywhere, and traditional pay TV services, as it drives incremental revenue and contributes to subscriber retention.”

This comment has been removed by a blog administrator.

ReplyDelete